2024 will see a global focus on disinflation-fuelled rate cuts, suppressed but steady economic growth and the return of political intrigue with US and UK elections on the horizon, according to Argentex’s latest FX Navigator report published today. The report explores how FX markets and currencies are set to perform in 2024.

The report, authored by Argentex’s Head of FX Analysis Joe Tuckey, notes that 2024 presents the “last mile” for the global 2% inflation target to be reached and that central banks will cut rates in line with disinflation. Timing and the extent of rate cuts will be a key factor driving FX moves this year. However, potentially increasing tensions in the Middle East could pose a risk to the disinflation narrative with higher energy prices.

The UK and US elections loom large for FX markets in 2024. In the UK, Labour’s assertion that they would integrate closer to Europe is seen as a potential sterling positive, whilst in the US, the return of Trump would likely reignite volatility after the relative calm of Joe Biden’s tenure. Markets may become particularly concerned if the Trump regime exits NATO and withdraws support for foreign wars, thus asserting more pressure on other economies to pick up the financial slack.

In terms of growth, the lag effect from the rate hikes of the last couple of years may still not be fully felt. Germany stands out as a weak growth performer and China’s post-Covid rebound has been disappointing, the report notes, and the UK’s “perennially low” expectations for growth means the bar remains low for an upside surprise – as seen in 2023. In 2024, however, the UK is set to outperform France and Germany.

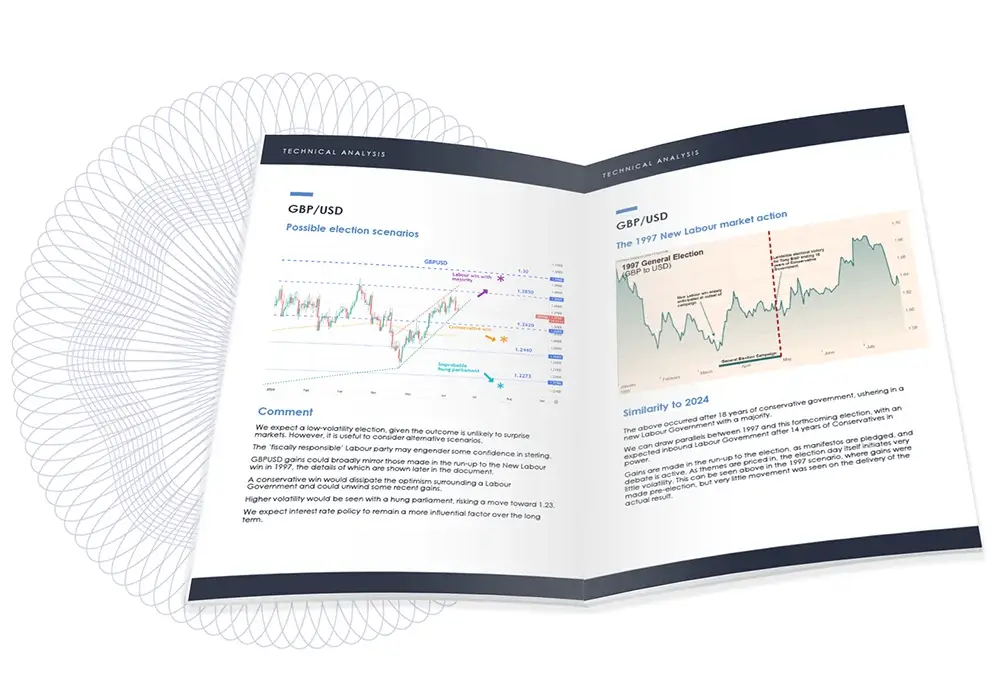

GBP/USD

Argentex’s base scenario for GBPUSD in 2024 suggests that sterling will manage to continue its recent resilience, incrementally edging higher as the dollar weakens. The Bank of England will retain a less dovish stance than the Fed, whilst economic data is likely to remain “unspectacular” but in line with moderate growth expectations of +0.5% to 1% growth in 2024.

The UK will once again manage to sidestep the annual doom-monger narratives, as rate cuts, falling inflation and low unemployment fuel a continuation of the drawn out post-Brexit recovery in the UK. Wage growth, alongside falling inflation, provides a boost for the UK consumer. As the general election, likely to be in Autumn, approaches, certain sterling positive themes may emerge and be priced in driven by manifesto pledges.

GBP/EUR

For GBPEUR, broad-based fundamental drivers for both currencies are likely to remain similar, with growth expectations of between +0.5% and 1%. Central banks are primed to make interest rate cuts through 2024, as disinflation steadily creeps toward 2%. Inbound data will likely be a mixed bag, depending on employment, energy prices, consumer behaviour and global demand themes.

However, the tendency for the Bank of England to be less dovish than the ECB may remain, as well as the potential for a post-General Election bounce later in the year.

EUR/USD

EURUSD saw historically low volatility in 2023 – the second-lowest price volatility on record. For 2024, Argentex predicts that the euro will remain at attractively low levels – in part due to Germany’s continually muted growth, but also if the eurozone suffers no fresh negative fundamental data. In 2023, Q4’s bounce showed that much of the bad news is already priced in for the euro, allowing for a recovery theme that may follow through this year. The labour market remains fairly strong, and as such, incomes remain solid and will only improve as disinflation continues. The euro will continue a gradual, incremental recovery, assisted by further unwinding dollar strength. Inflation in the services sector may delay the first rate cut.

Commenting, Argentex’s Head of FX Analysis, Joe Tuckey, said:

“If FX markets in 2022 were a flame-spitting Lamborghini, 2023 was more akin to a Volvo 4×4: safe, slow and steady. As disinflation eventually took hold, FX volatility imploded, and the dollar weakened.

“This year, the comparative timing and extent of rate cuts between major central banks will be paramount to FX markets. The US economy may finally slow, just as the UK, Europe and China find their footing. World growth is expected at between 2 and 3%, whilst 2024 FX will absorb the ramifications of one of the most significant electoral years in recent history, with some 40% of the world’s population going to the polls from the USA to Russia, India to South Africa and beyond.”

For more information about Argentex’s payments and currency risk management solutions, please contact us on [email protected].